Property Mortgages in the UAE Explained

June 10, 2025

Buying property in the UAE is an increasingly attractive prospect for both residents and foreign investors. However, due to high upfront costs, most buyers depend on mortgage financing to afford their dream homes or investment properties. Understanding the property mortgage Dubai, Abu Dhabi and generally UAE home financing laws, is critical for navigating the application process, evaluating costs, and securing the best interest rates.

This guide breaks down everything you need to know, from available mortgage types to step-by-step procedures on how to get a mortgage in the UAE, tailored for both residents and non-residents of the UAE.

Dubai’s mortgage market saw strong activity in Q1 2025 with a 4.76% uptick in transactions.

Total mortgage value rose by an impressive 32% between January and February.

It’s great that so many people want to get a foot on our Emirate’s property ladder.https://t.co/v7lQpv3rmg

— Amira Sajwani (@Amira_H_Sajwani) April 25, 2025

A property mortgage is a loan provided by a bank or financial institution that allows you to purchase real estate while repaying the amount borrowed over time, with interest. The UAE mortgage system is well-regulated by the Central Bank of the UAE, ensuring borrower protection and lender transparency.

🔗 Central Bank Mortgage Guidelines

Here are the most common types:

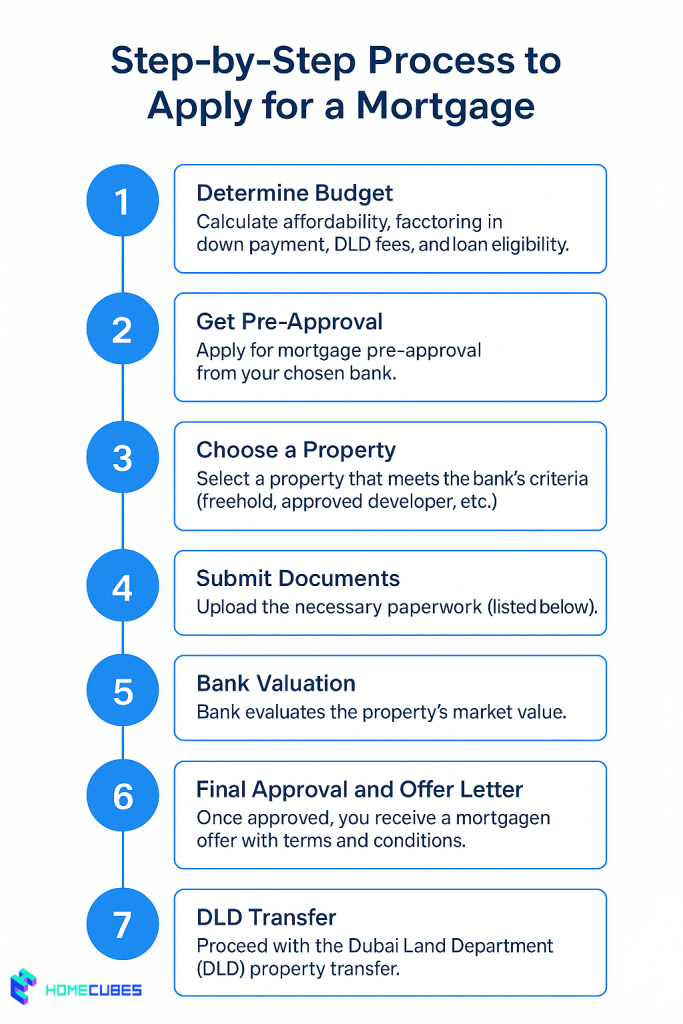

To qualify for a mortgage in the UAE, you typically must meet these minimum requirements:

| Criteria | Resident | Non-Resident |

| Minimum Age | 21 years | 21 years |

| Income | AED 15,000/month | AED 25,000/month or equivalent |

| Credit Score | 580+ (AECB) | International banking history required |

| Down Payment | 20–25% | 25–35% |

| Loan Tenure | Up to 25 years | Up to 20 years |

🔗 Check your AECB Credit Score

🔗 DLD Mortgage Registration Guide

Non-residents can obtain a mortgage for properties in designated freehold zones, but the conditions are stricter:

🔗 Bayut Guide to Non-Resident Mortgages

Sharia-compliant mortgages are profit-based, not interest-based. These are commonly structured as:

Offered by:

These are ideal for buyers seeking halal investment structures.

Refinancing lets you switch to a better rate or adjust your repayment term. Common reasons include:

Before refinancing, ensure the new bank covers:

Profile: Sara, a 32-year-old marketing executive

Goal: Buy a 1BR apartment in Al Reem Island

Monthly Salary: AED 18,000

Bank Chosen: First Abu Dhabi Bank (FAB)

Outcome: Fixed rate of 3.8% for 5 years, no penalties for early closure after 3 years.

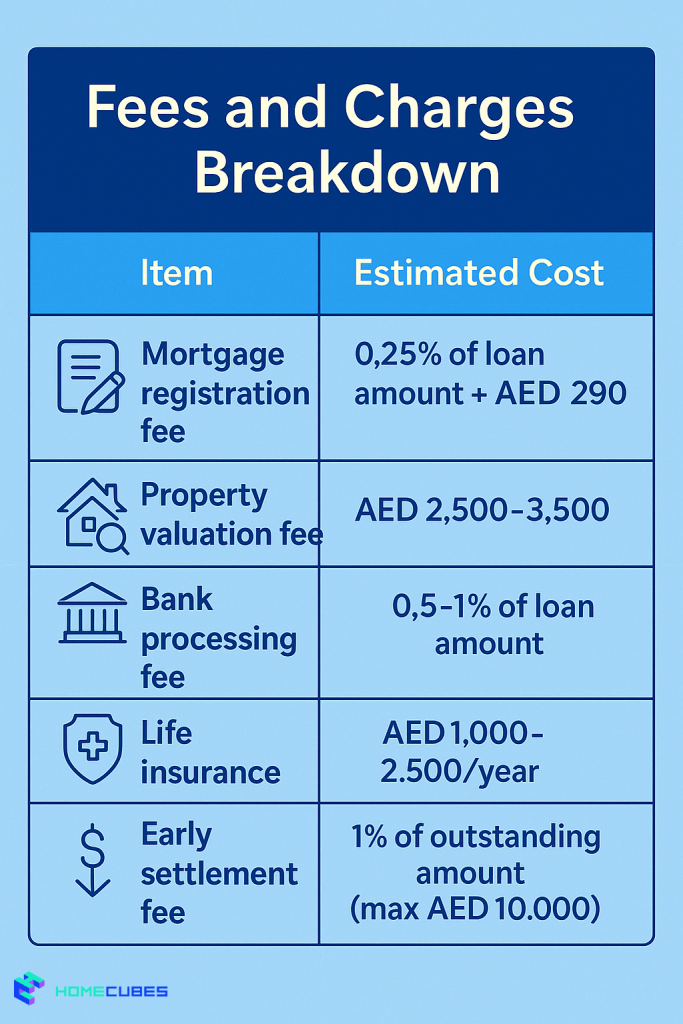

| Item | Estimated Cost |

| Mortgage registration fee | 0.25% of loan amount + AED 290 |

| Property valuation fee | AED 2,500–3,500 |

| Bank processing fee | 0.5–1% of loan amount |

| Life insurance | AED 1,000–2,500/year |

| Early settlement fee | 1% of outstanding amount (max AED 10,000) |

🔗 Dubai Land Department Fee Structure

Yes, based on property ownership laws for foreigners in UAE you can get mortgage, but you’ll need to meet higher down payment and income requirements. Only freehold areas are allowed.

Up to 25 years for residents, and generally 15–20 years for non-residents.

Yes, joint mortgages are allowed for legally married couples.

No. The UAE has no personal income tax, so mortgage interest deduction does not apply.

Yes, many banks offer mortgage buyouts, often covering part of the transfer costs.

Mortgage trends in the UAE are shifting toward digitalization and flexible repayment models. The rise of fintech mortgage brokers, instant approval systems, and tokenized mortgage platforms is shaping the next generation of property financing.

Additionally, initiatives like Dubai’s Open Finance Strategy and digital KYC integration with DubaiNow and Emirates Blockchain Platform are making mortgage transactions faster and safer.

At Homecubes, we’re building tools to bridge the gap between traditional real estate and the tokenized property economy. While we are currently awaiting regulatory approval from VARA for our real estate tokenization platform, our mission is to simplify property investment, including future mortgage-backed token offerings.

📩 Reach out to Homecubes and join our early access list. Be the first to explore fractional real estate opportunities, compliance education, and mortgage tokenization updates once we’re live.

Table of Contents Introduction Global Demand Dubai Real Estate – Snapshot Why Dubai Stands Out…

Dubai’s real estate market has moved from a speculative frontier to a globally recognized hub…

Table of Contents Introduction Market Overview: H1 2025 by the Numbers Key Drivers Behind the…