Mortgage vs. Payment Plan: Key Differences

July 18, 2025

Dubai’s real estate market is known for its accessibility to both local and international buyers, supported by a wide range of financing options. But when it comes to choosing how to finance your property, one of the most critical decisions you’ll make is whether to opt for a bank mortgage or a developer-offered payment plan.

This decision isn’t simply about which path is cheaper or faster—it’s about aligning your financing method with your long-term goals, risk tolerance, cash flow, and the type of property you’re targeting.

For instance, if you’re buying a ready-to-move-in apartment in Downtown Dubai, a mortgage might be the only viable path. On the other hand, if you’re investing in an off-plan project in Dubai South, a flexible payment plan from the developer may make more financial sense.

Flexible payments, lesser fees: How Dubai’s new initiative benefits first-time home buyershttps://t.co/C3pv0cJlaJ

— Khaleej Times (@khaleejtimes) July 6, 2025

In this comprehensive guide, we’ll break down the key differences between mortgages and payment plans, including eligibility criteria, interest considerations, risk profiles, and when each option makes the most sense. Whether you’re a first-time buyer or a seasoned investor, this article will help you make an informed, strategic decision.

A mortgage is a financial arrangement where a buyer borrows funds from a bank or licensed financial institution to purchase a completed or under-construction property. The buyer typically pays a down payment upfront (20–40%), and the remainder is paid over a fixed term ranging from 5 to 25 years.

A developer payment plan is a financing model where the real estate developer offers the buyer a schedule to pay for the property over time—without involving a bank or lender.

Unlike mortgages, these plans are not regulated by financial institutions and typically do not charge interest—though the total price of the unit may be higher to account for this.

For a detailed overview of available plans, visit Bayut’s guide to off-plan properties and areas across Dubai..

| Feature | Mortgage | Developer Payment Plan |

| Regulator | UAE Central Bank, DLD | Developer (no external regulation) |

| Eligibility | Based on credit score, salary, income | Minimal eligibility |

| Property Type | Ready or resale units | Off‑plan only |

| Interest | Yes (bank interest applies) | No interest, but pricing may be higher |

| Tenure | 5–25 years | 1–5 years (tied to delivery) |

| Risk | Interest hikes, penalties | Delays, developer risk |

| Flexibility | High (refinancing available) | Low (fixed with limited exit options) |

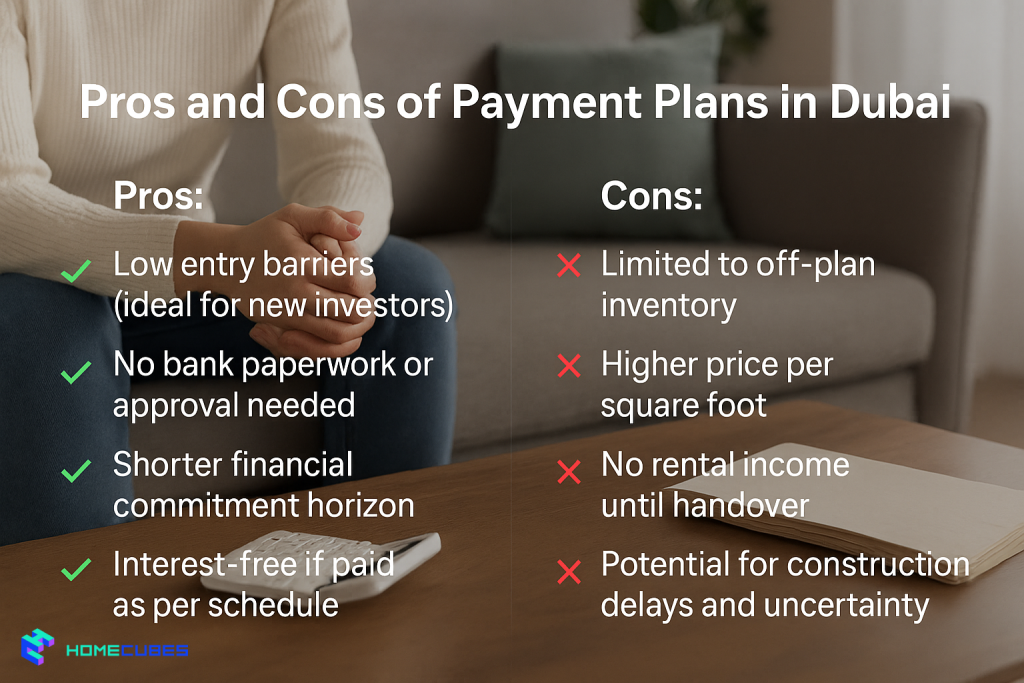

The advantages and drawbacks of off-plan payment plans in the UAE are briefly outlined down here:

Mortgages are best for:

Developer payment plans are ideal for:

Conclusion:

Mortgage ensures instant returns but demands higher upfront commitment. Payment plan defers income but allows market entry with lower cash.

| Fee Type | Mortgage | Payment Plan |

| DLD Registration | 4% of property value | 4% at handover |

| Valuation Fee | AED 2,500–3,500 | N/A |

| Processing Fee | 0.5–1% of loan | N/A |

| Mortgage Registration Fee | 0.25% of loan amount | N/A |

| Insurance | Mandatory (property + life) | Not required or embedded |

| Post-Handover Risk | Rate hikes, default risk | Delay in delivery, no rental |

Yes—but only if the developer and project are bank-approved and at least 50% completed.

Technically yes, but the developer may embed financing cost into the property price.

Yes—many buyers refinance their payment plan into a mortgage post-handover.

For mortgages, it affects your credit score and may lead to repossession. With payment plans, developers may forfeit deposits or cancel contracts.

The debate between mortgage vs payment plan Dubai reflects broader financial and lifestyle preferences. If you’re looking for immediate possession, rental income, and a wider range of property options, a mortgage might be your best bet—especially if you’re financially stable and eligible for bank approval.

On the other hand, if your goal is to enter the market with minimal capital, especially in the off-plan segment, a developer payment plan may provide a more accessible, flexible route. In this case, make sure to learn how to manage delays in off-plan property handovers, in case it happens.

However, the key is not just choosing the easier path—but the one that aligns with your cash flow, risk appetite, property goals, and investment timeline. Mortgages require deeper planning, but they enable stronger long-term ownership. Payment plans minimize risk upfront but require confidence in the developer and delayed returns.

No matter which path you take, due diligence, legal clarity, and planning for the full ownership lifecycle are critical.

At Homecubes, we believe informed buyers make better investments. While our real estate tokenization platform is currently awaiting its official license from the Dubai Virtual Assets Regulatory Authority (VARA), we’re committed to offering accurate insights, comparisons, and financing guidance.

📩 Interested in financing options, co-investment strategies, or tokenized real estate?

Contact our team to learn more and receive updates when our platform goes live.

Table of Contents Introduction Global Demand Dubai Real Estate – Snapshot Why Dubai Stands Out…

Dubai’s real estate market has moved from a speculative frontier to a globally recognized hub…

Table of Contents Introduction Market Overview: H1 2025 by the Numbers Key Drivers Behind the…