The Impact of Blockchain on Mortgage Securitization in Dubai

December 16, 2024

Blockchain technology has the potential to transform various industries, and the mortgage securitization market in Dubai stands to benefit greatly. This article explores how blockchain is reshaping mortgage securitization in Dubai, highlighting its benefits, challenges, and future outlook. Blockchain’s ability to increase transparency, reduce costs, and streamline processes addresses many inefficiencies currently present in Dubai’s mortgage and real estate sectors.

Real World Asset Launches Mortgage-Backed Stablecoin On XRP Ledger – Benzinga https://t.co/yeFcwY9qpG

— Digital Asset Investor (@digitalassetbuy) June 27, 2023

Mortgage securitization refers to pooling various individual mortgages and creating mortgage-backed securities (MBS). These MBS are then sold to investors. This process allows financial institutions to offload risk and provides investors with an opportunity to invest in real estate without owning physical property.

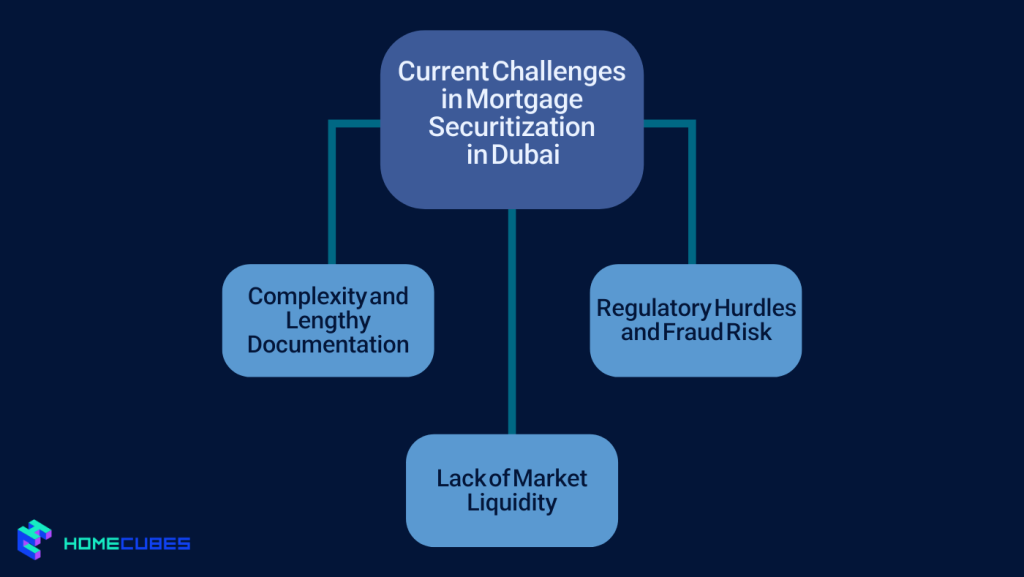

Dubai’s mortgage-backed securities (MBS) market has grown in recent years, driven by the expansion of the real estate sector. However, the process remains complicated, marked by inefficiencies, lengthy documentation, fraud risks, and a lack of transparency. The securitization process in Dubai is still developing, with the traditional methods failing to keep pace with the needs of the market.

Blockchain is a decentralized, distributed ledger technology that records transactions across a network of computers in a secure and immutable way. Unlike centralized systems, blockchain uses consensus mechanisms to validate and record transactions, ensuring transparency, security, and traceability.

In mortgage securitization, blockchain provides a transparent and secure method for recording every stage of a mortgage’s life cycle. All transactions, including loan origination, repayment, and ownership transfers, are tracked on a decentralized ledger. Smart contracts—self-executing contracts with terms written directly into the code—can automate processes such as loan repayments, asset transfers, and payment distributions.

The traditional mortgage securitization process in Dubai involves numerous intermediaries, including banks, real estate agents, and insurers. Each intermediary must verify document information, causing delays and increasing administrative costs.

Dubai’s mortgage sector is governed by the Central Bank of the UAE. While these regulators maintain market stability, they can also create complexity. Fraud risks arise from inaccuracies in property titles and mortgage documentation, and a lack of market liquidity reduces investor confidence.

The mortgage-backed securities market in Dubai is still developing, limiting liquidity and making it harder for investors to easily buy and sell MBS. This reduces market efficiency and investor interest.

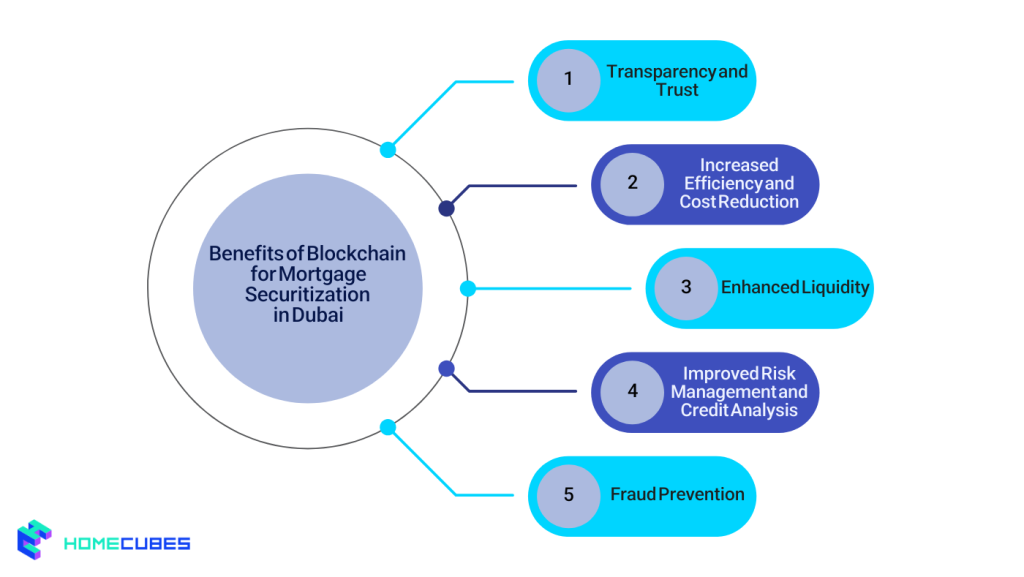

Blockchain increases transparency by providing an immutable, public ledger for every transaction. Each transaction is recorded in real time, making it easier to verify property ownership, loan histories, and payments.

Blockchain reduces cost in Dubai property selling and buying, by reducing reliance on intermediaries through providing a decentralized system where participants can access shared information. This feature also streamlines the mortgage securitization process, cutting down on paperwork, verification delays, and administrative costs.

Blockchain allows for the fractionalization of mortgage-backed securities. Large assets, such as MBS, can be divided into smaller, more tradable units, making them more accessible to a broader range of investors. Thus, blockchain can be a solution for property liquidity challenges in Dubai as well as large assets such as MBS.

Blockchain provides a transparent and real-time view of mortgage performance, allowing investors to assess risk more accurately. Detailed records of payment histories and borrower statuses offer a better understanding of potential defaults.

Blockchain’s decentralized nature makes it resistant to fraud. All transactions are encrypted and recorded on a public ledger, making it nearly impossible to alter historical data without being detected.

Dubai’s commitment to blockchain adoption, exemplified by the Dubai Blockchain Strategy, shows promise. However, the legal and regulatory frameworks for blockchain-based mortgage securitization are still in development.

Dubai’s real estate and financial systems are based on traditional methods that rely heavily on intermediaries. Moving to a blockchain-based model requires integrating new technologies into these legacy systems, which could meet resistance from stakeholders accustomed to the existing process.

To fully implement blockchain in mortgage securitization, Dubai will need to establish robust technological infrastructure. This includes ensuring the security and scalability of the blockchain platform, as well as addressing any potential cybersecurity risks.

As blockchain technology matures and regulatory clarity improves, Dubai is well-positioned to become a leader in blockchain-based mortgage securitization in the Middle East.

Dubai’s status as a global financial hub makes it an ideal location for attracting international investors. Blockchain’s transparency and efficiency could appeal to global investors seeking secure and accessible ways to invest in the city’s real estate sector.

As blockchain adoption grows, Dubai’s regulatory bodies, such as the DFSA and DLD, will likely update their frameworks to accommodate blockchain technology. Clear regulations will help ensure that blockchain-based transactions in mortgage securitization are legally enforceable.

Blockchain technology offers significant potential to improve the mortgage securitization process in Dubai. By enhancing transparency, increasing market liquidity, and reducing costs, blockchain can address many inefficiencies in the current system. However, overcoming challenges related to regulation, integration with existing systems, and technology will be crucial for the widespread adoption of blockchain in mortgage securitization. With Dubai’s ongoing commitment to innovation and digital transformation, blockchain could play a pivotal role in shaping the future of mortgage securitization in the city, contributing to the growth and efficiency of its real estate market.

Homecubes as a licensed blockchain-based platform has got exciting real estate tokenization projects in the Dubai real estate market. Contact us with confidence or further information on our lucrative fractional investment opportunities in prime properties across Dubai.

Table of Contents Introduction Global Demand Dubai Real Estate – Snapshot Why Dubai Stands Out…

Dubai’s real estate market has moved from a speculative frontier to a globally recognized hub…

Table of Contents Introduction Market Overview: H1 2025 by the Numbers Key Drivers Behind the…