Sharia-Compliant Mortgage Options in the UAE: A Complete Guide

July 19, 2025

The UAE has become a thriving hub for Islamic finance, offering innovative and flexible Sharia-compliant home financing options for both residents and international investors. An Islamic mortgage in the UAE is structured to comply with Islamic law, which prohibits riba (interest). Instead of charging interest, banks use alternative structures based on partnership, leasing, or profit margin.

#BREAKING: What is a halal mortgage?

Islamic mortgages are mortgages that are Sharia law compliant. They differ from traditional home loans in that you don’t pay interest as this is forbidden under Sharia law. Making money from loans goes against Islamic beliefs. #cdnpoli pic.twitter.com/GTdTGjCTSa— Jayme Knyx (@JaymeKnyx) April 17, 2024

As the real estate market continues to attract Muslim and non-Muslim investors seeking ethical finance, understanding how these products work can help you make a more informed choice. We would also like to recommend you to make yourself familiar with the real estate market in Dubai, using platforms like DXB interact; Dubai real estate platform.

Islamic home finance is built on the following Sharia principles:

These principles ensure a more ethical and transparent financing structure for buyers in the UAE.

| Feature | Islamic Mortgage | Conventional Mortgage |

| Interest | Not allowed; profit-based | Based on fixed or variable interest |

| Ownership Structure | Shared or leased | Owned with lien by bank |

| Legal Framework | Sharia Law + UAE Civil Law | UAE Civil Law only |

| Flexibility | Fixed profit margin, no compounding | Compounding interest possible |

Unlike conventional mortgages, Islamic mortgages do not involve lending money in exchange for interest. Instead, the bank purchases the property and either resells or leases it to the buyer.

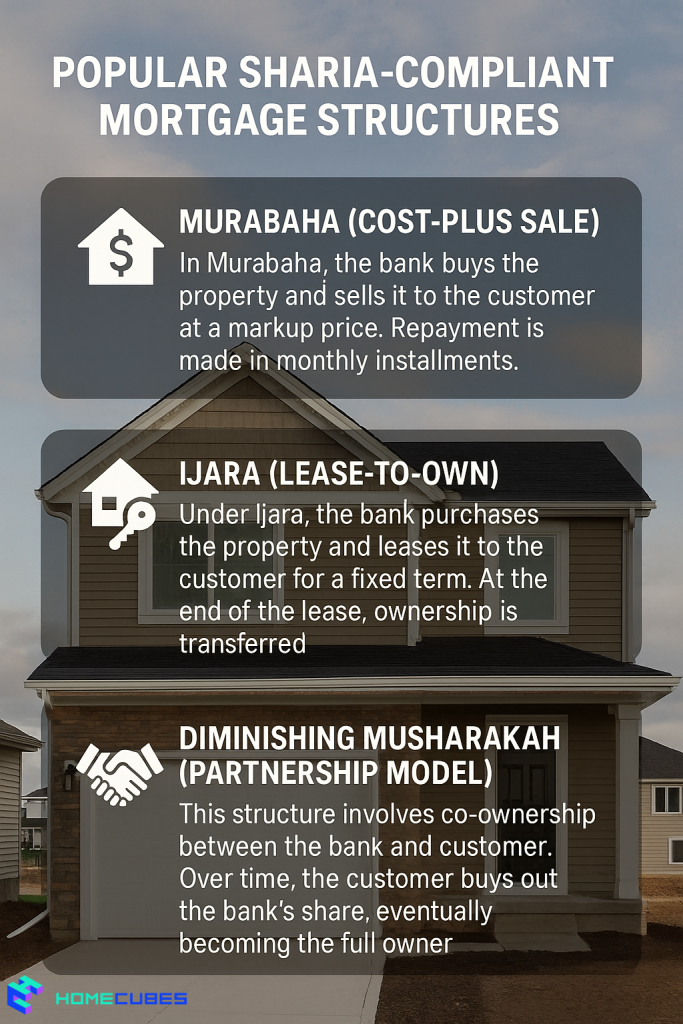

In Murabaha, the bank buys the property and sells it to the customer at a markup price. Repayment is made in monthly installments.

Under Ijara, the bank purchases the property and leases it to the customer for a fixed term. At the end of the lease, ownership is transferred.

This structure involves co-ownership between the bank and customer. Over time, the customer buys out the bank’s share, eventually becoming the full owner.

Here are some leading UAE banks offering Sharia-compliant mortgage products:

DIB offers various home finance solutions, including Ijara and Diminishing Musharakah. Their Sharia-compliant mortgages are known for flexible tenures and high finance-to-value (FTV) ratios. Visit DIB

ADIB provides Islamic home financing through Ijara structures with fixed or variable rental rates. It supports both UAE nationals and expatriates.

Visit ADIB

Offers attractive financing options for salaried and self-employed individuals using Ijara and Murabaha. Their products are approved by their Internal Sharia Board.

Visit Emirates Islamic

SIB provides up to 90% financing with flexible terms, including a Murabaha structure and life Takaful coverage.

Visit SIB

Most banks have similar requirements, including:

To make things easier, you can check your credit score in Dubai or across the country, to ensure that you have the initial requirements for going through the mortgage process.

Despite their ethical appeal, Islamic mortgages may come with certain challenges:

Always review the fine print and consult with a Sharia advisor or financial expert before committing.

Scenario: A 35-year-old expat opts for an Ijara-based Islamic mortgage through Emirates Islamic Bank to buy a ready apartment in Jumeirah Village Circle.

Outcome: Over time, the buyer pays down the bank’s share and acquires full ownership without paying interest, aligning with personal and religious values.

| Fee Type | Approximate Cost (AED) |

| Processing Fee | 1% of finance amount (up to AED 10,000) |

| Property Valuation | AED 2,500–3,500 |

| Takaful Insurance | Based on finance value and age |

| DLD Registration | 4% of property value |

| Ijara Agreement Drafting | AED 2,000–3,000 |

| Early Settlement | 1% of remaining amount (capped at AED 10,000) |

These charges are generally similar to those in conventional mortgages, except that Sharia-compliant financing includes Takaful (Islamic insurance) instead of conventional mortgage insurance.

Q1: Can non-Muslims apply for Islamic mortgages in the UAE?

Yes. Islamic finance is open to all residents and investors regardless of religion.

Q2: Is profit margin negotiable in Islamic mortgages?

In some cases, yes. Banks may offer different rates based on your creditworthiness or income.

Q3: Is there a fixed or variable profit option?

Yes. Many banks offer both fixed and variable rate profit margins depending on the product.

Q4: Are Islamic mortgages available for off-plan properties?

Rarely. Most Islamic financing options are limited to completed or ready properties.

Q5: Can I refinance a conventional loan with an Islamic mortgage?

Yes. Some banks offer conversion options to switch from conventional to Islamic financing.

At Homecubes, we understand the growing demand for Islamic mortgage UAE options. Our platform is designed to help future investors identify and explore ethical, Sharia-compliant opportunities across Dubai and the wider UAE. While we are currently in the final stages of securing our real estate tokenization license from VARA, we are building a robust foundation to support your goals.

If you’re seeking compliant, transparent, and smart property investment strategies, get in touch with Homecubes and stay informed as we prepare to launch innovative solutions tailored for ethical and fractional real estate investing.

Table of Contents Introduction Global Demand Dubai Real Estate – Snapshot Why Dubai Stands Out…

Dubai’s real estate market has moved from a speculative frontier to a globally recognized hub…

Table of Contents Introduction Market Overview: H1 2025 by the Numbers Key Drivers Behind the…